By Pete Pennicott | December 8, 2024

By Pete Pennicott | December 8, 2024

November lay witness to a ‘red wave’ Republican sweep of the presidency and the Congress, not to mention winning the popular vote. The swift and decisive victory by the incoming Trump administration removed the substantial uncertainty that had been building in the weeks before the election and paved the way for markets to stage another strong rally. Analysts estimated that the proposed corporate tax cut would boost earnings by up to 5%, which ensured that all major US indices reached new highs as investors paid little regard to rich valuation metrics.

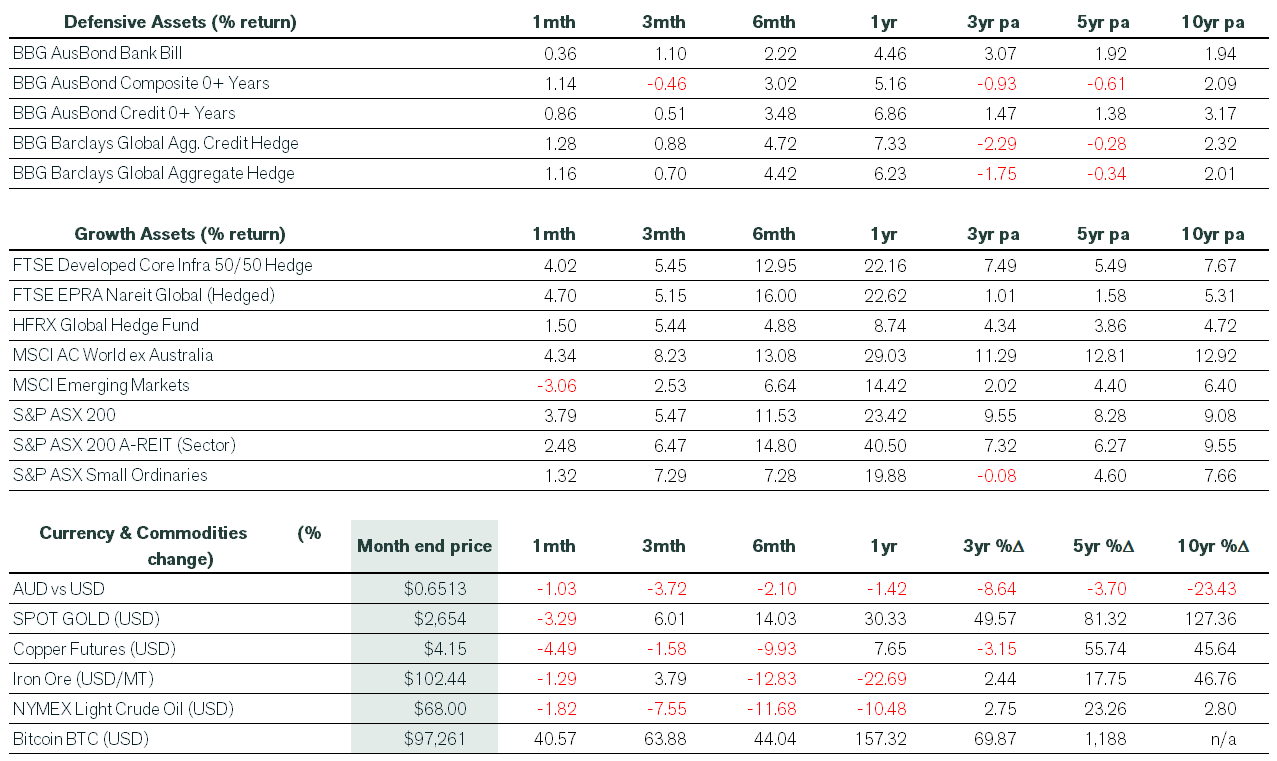

The MSCI ACWI ex-Australia index delivered a total return of 4.3% to domestic investors in November, led by a strong rally in US equities. The benchmark US S&P 500 posted its best month of 2024, returning nearly 6%, including dividends in local currency. Meanwhile, the small-cap Russell 2000 posted its best monthly gain since December 2023, generating a lofty 11% total return. The Nasdaq Composite returned 6.3%, while the Dow Jones Industrial Index returned 7.7%.

However, the ongoing US dollar strength has put another dent in emerging market equities, losing 3% in Australian dollar terms. The declines were broadly based across Asia and Latin America. Over the last ten years, emerging market equities have delivered less than half the return of their developed nation peers. On a brighter note, hedged returns for global property and infrastructure printed with a 4-handle, as real assets benefited from the sharp decline in real yields in late November. Returns in this space have exceeded 20% over the last twelve months, but remain more muted over longer time horizons.

On the domestic front, the ASX 200 finished the month 3.8% higher, reversing its October losses. Despite the risk-on sentiment, domestic small caps struggled to keep pace with their large cap peers, managing to return 1.3% for November.

Despite wild fluctuations in bond yields, fixed most income markets generally performed positively in November. In the US, the strong growth outlook for corporate earnings saw spreads tighten slightly in investment-grade corporate bonds, with more significant gains in the high-yield space. Agency mortgage-backed securities (MBS) showed signs of recovery, while municipal bonds outperformed Treasurys. Elsewhere, Japanese government bonds continued to underperform due to market expectations of further rate hikes and faster balance sheet reductions in 2025. On the domestic front, the fall in treasury yields was sharper than global peers as ongoing weak economic data helped the composite bond index outperform higher-risk credit indices.

The US dollar strengthened further in light of Trump’s ‘America First’ approach to economic and foreign policy. The US Dollar Index (DXY), which tracks the greenback’s value against a basket of major currencies (such as the euro and the yen), gained nearly 2% after rallying by more than 3% in October. The Australian dollar lost just over 1% versus the US dollar in November.

The US dollar prices of gold, copper, iron ore and crude oil all moved lower during the month.

Finally, crypto posted spectacular gains, with Bitcoin surging by 40% to test the psychological $100,000 mark. The cryptocurrency reached new all-time highs during the month, easily surpassing its previous record set in November 2021. Trump’s re-election victory was a major driver, as investors anticipated a more crypto-friendly regulatory environment and potential institutional adoption of the cryptocurrency.

Australia

On the economic front, the Reserve Bank of Australia (RBA) held interest rates steady in November at 4.35%. The RBA’s quarterly monetary policy statement said the economy was still operating “above capacity”. It projects underlying inflation to move below 3% in mid-to late-2025 and to 2.5% in late 2026. The RBA has maintained it wants to see inflation “sustainably“ in its target band before cutting rates. Labour market data printed softer than expected for October, but the trend data remained strong.

Global

The US Federal Reserve (the Fed) continued to normalise monetary policy despite ongoing economic growth and above-target inflation, cutting the Fed Fund’s target rate by 0.25% to 4.50‐4.75%. Chairman Jerome Powell said the US economy was performing remarkably well, with inflation cooling off, and reiterated that interest rate policy remains data dependent. The Fed’s preferred inflation index, the PCE Price Deflator, printed in line with modest consensus expectations, while personal income easily beat the analyst consensus. Also, October headline retail sales came in higher than expected, with significant upward revisions to September’s data.

Elsewhere, annual inflation in the Eurozone accelerated for a second month to 2.3% in November as last year’s sharp declines in energy prices rolled off. Meanwhile, core inflation remained at 2.7%.

In China, annual retail sales jumped 4.8% in October, exceeding consensus of 3.8%. It was the fastest growth in retail turnover since February, boosted by a week-long holiday and a recent shopping festival. Overall, annual inflation in China remains low, and house prices are still falling.

If you want to discuss any of the above information or your personal investment strategy, then book a chat with your financial adviser here.

Pete is the Co-Founder, Principal Adviser and oversees the investment committee for Pekada. He has over 18 years of experience as a financial planner. Based in Melbourne, Pete is on a mission to help everyday Australians achieve financial independence and the lifestyle they dream of. Pete has been featured in Australian Financial Review, Money Magazine, Super Guide, Domain, American Express and Nest Egg. His qualifications include a Masters of Commerce (Financial Planning), SMSF Association SMSF Specialist Advisor™ (SSA) and Certified Investment Management Analyst® (CIMA®).