By Pete Pennicott | February 3, 2023

By Pete Pennicott | February 3, 2023

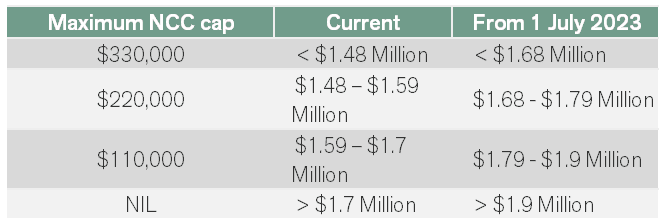

As a result of the CPI figure released in January, the General Transfer Balance Cap (TBC) will increase from $1.7 million to $1.9 million from 1 July 2023.

This increase will have flow-on impacts on superannuation contribution limits and strategies.

The transfer balance cap is the limit on the amount of superannuation that you can transfer from accumulation phase to retirement phase income streams.

Retirement phase income streams include all superannuation income streams except:

Important to note that earnings, losses or income stream payments do not impact the transfer balance account.

It depends. Due to how an individual’s personal transfer balance cap (TBC) is calculated using a proportional indexation approach, the impact will range from a full increase of $200,000 to no change.

Let’s take two extreme examples:

Depending on your situation, there may be no impact from these changes. If you are considering using bring forward non-concessional contribution provisions or commencing a retirement phase income stream, then it would be beneficial to assess the difference in outcomes if taking action before or after 1 July 2023.

If you have any questions or want to chat about your situation and how the increases to the transfer balance cap might impact you, then please book a chat here.

Pete is the Co-Founder, Principal Adviser and oversees the investment committee for Pekada. He has over 18 years of experience as a financial planner. Based in Melbourne, Pete is on a mission to help everyday Australians achieve financial independence and the lifestyle they dream of. Pete has been featured in Australian Financial Review, Money Magazine, Super Guide, Domain, American Express and Nest Egg. His qualifications include a Masters of Commerce (Financial Planning), SMSF Association SMSF Specialist Advisor™ (SSA) and Certified Investment Management Analyst® (CIMA®).